Associate professor, Ph.D Pasko O.

Sumy National Agrarian

University, Sumy, Ukraine

THE NEWLY INTRODUCED CONCEPT OF KEY AUDIT MATTERS IN INTERNATIONAL

STANDARDS ON AUDITING

The turning

point in transformation of the International Standards on Auditing in truly

global standards was so called Clarity Project. On February 27, 2009, the

Clarity Project reached its completion when the Public Interest Oversight Board

approved the due process for the last several clarified ISAs. Auditors

worldwide will now have access to 36 newly updated and clarified ISAs and a

clarified International Standard on Quality Control (ISQC)[1].

After its completion the IAASB decided for several years not to change pronouncements

in order to secure adaption and implementation of newly clarified ISA’s. Today

we have 2013 AD and growing activities of IAASB toward improvements of its

standards. In Handbook 2012 IAASB included two new revised standards, namely

ISA 315 and ISA 610. These standards introduced some minor amendments relating

to work of internal auditors. In active project IAASB by the time are changes

to ISA 700 and new ISA 701. Among all mentioned standards the biggest changes

is believed will be made to auditor’s report, through ISA 700 (revised) and new

ISA 701. In this paper we are going examine the newly introduced concept of key

audit matters, previously known as auditor commentary.

Let’s begin with the definition, given in

proposed ISA 701: кey audit matters - those matters that, in the auditor’s professional

judgment, were of most significance in the audit of the financial statements

[1,с.3].

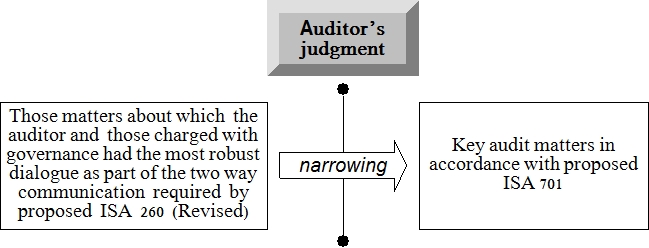

Users of

the financial statements have indicated they have an interest in those matters

about which the auditor and those charged with governance had the most robust

dialogue as part of the two way communication required by proposed ISA 260 (Revised)

and have called for additional transparency about those communications. Key

audit matters are some kind of whistle-blowing of the matters which in the

cource of audit auditor discussed with THWG. Revealing such information “is

intended to provide users of the financial statements with additional information

to enhance their understanding of the audit” [1,с.2].

The auditor

shall communicate those matters in a separate section of the auditor’s report under

the heading “Key Audit Matters”, and include appropriate subheadings for each

of the key audit matters communicated.

ISA 701

emphasizes, what communicating key audit matters in the auditor’s report is not

intended to: (a) Express an opinion on individual accounts or disclosures; or

(b) Be a substitute for the auditor expressing a qualified opinion or an adverse

opinion when required by the circumstances of a specific audit engagement [1,с.6].

What is to

be included in key audit matters? Proposed ISA 701 clearly states what key

audit matters are, in all cases, a selection of matters communicated with those

charged with governance [1,с.3]. “The auditor’s decision-making process is therefore

designed to narrow the matters discussed with those charged with governance to

a smaller number of matters based on the auditor’s judgment about which matters

were of most significance in the audit» [1,с.6] (fig.1).

Fig. 1. The Auditor’s Process

to Determine Key Audit Matters according to proposed ISA 701

The matters

to be communicated are based on the auditor’s professional judgment and are influenced

by the nature and extent of matters communicated with those charged with governance

in accordance with proposed ISA 260 (Revised).

In determining

whether a matter is communicated as a key audit matter, the auditor shall use

professional judgment, taking into account the nature and extent of communications

with those charged with governance, including, at a minimum: 1) Whether the

matter was identified as, or is related to, a significant risk in accordance

with ISA 315; 2) The degree of difficulty encountered in obtaining sufficient

appropriate audit evidence about the matter; 3) The difficulty of the judgment

involved relating to the matter; 4) Whether the auditor identified a

significant deficiency in internal control relating to the matter (ІSA 701.11) [1,с.3].

Notwithstanding

ISA 701 applies to auditors of listed entities, it may be applied, adapted as

necessary in the circumstances, for audits of entities other than listed

entities. Auditors of entities other than listed entities may include a

discussion of key audit matters in the auditor’s report. In such circumstances,

the auditor shall discuss doing so as part of agreeing the terms of the audit engagement

in accordance with ISA 210. As states ISA 701: «Communication about the

possibility of including a discussion of key audit matters in the auditor’s

report at the commencement of the audit ensures that management and those

charged with governance are aware of the auditor’s ability to do so» [1,с.14].

The number

of matters to be included in the auditor’s report is affected by the size and

complexity of the entity, the nature and conditions of its business, and the

facts and circumstances of the audit engagement. According to ISA 701 a range

of two to seven matters may generally be appropriate.

1. Proposed International Standard on

Auditing (ISA) 701 Communicating Key Audit Matters in the Independent Auditor’s

Report [Electronic resource] // International Federation Of Accountants. - Mode

of access: WWW.URL: http://www.ifac.org/sites/default/files/meetings/files/20130415-IAASB-Agenda_Item_2C-Proposed_ISA_701-final.pdf. - Last access: 2013. – Title from

the screen.