Economics / 7. Accounting and Auditing

Ekaterina Erokhina

Postgraduate

studies, First year of study, Peoples’ Friendship University of Russia

Moscow, Russian Federation

International Standards on Auditing and

Developing approaches the performance assessment requirements of auditing

standards regulating organization of auditors in Russia

International auditing

standards are specific recommendations for all aspects of auditing sphere. Such

recommendations prepare The International Federation of Accountants (IFAC). The

main idea of these standards – to develop a final recommendation is to

standardize processes and audit criteria for audit services rendered.

Currently, IFAC included

157 members and associates in 123 countries, representing more than 2.5 million

accountants and auditors. Organization - IFAC members participate in the

program compliance, thereby demonstrating its interest in strengthening the

high standards of accountants worldwide.

Compliance program consists

of 3 parts:

Ø

Part 1 - recognition of regulatory IFAC

values in the standardization activities of professional

accountants and auditors.

Ø

Part 2 - A self-assessment

procedures IFAC member’s own efforts to promote international standards and

control their execution.

Ø

Part 3 - declare action plan to

implement in their practice of existing international standards with an

indication of the selected tools and provide resources and procedures. Also,

the Plan of auditor’s procedures should reflect the regulatory changes in the

internal standards of IFAC member bodies, related to the promotion of

international standards and the achievement of the required level of compliance

with them.

The Russian Federation is

represented by two IFAC professional audit associations: Russian Collegium of

Auditors (RCA) and the Institute of Professional Accountants of Russia (IPAR).

International auditing

practices are based on International Standards of Accounting and Reporting ,

International Standards on Auditing and audit-related services , the provisions

of the International Auditing Practices , as well as international norms of

accounting education and ethics.

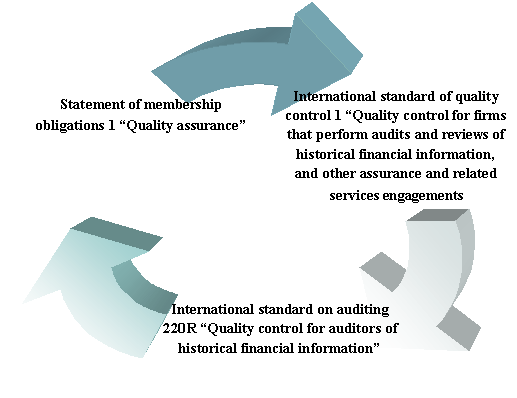

In the international

approach to ensure quality of audit services put 3 standards. (See Fig. 1.1.1).

Consider their appointment more.

Figure 1 - List of international standards and quality

control provisions audit

Source: Compiled by author

Fundamental document - «The obligation of

organizations - members of IFAC 1 «Quality Assurance ", is adopted by the

IFAC Council. Its purpose is to establish the responsibilities for the

professional associations related to the development and execution of test

programs to ensure the quality of work in an auditing firm to audit the

accounts of customers. These standard requirements are indicated on scoping

audit, and the approach to the formation of the verification period and

appropriate audit procedures. Standard represents the ethical principles and

requirements for professional competence. Next Article - International Standard

on Quality Control 1 «Quality Control for firms conducting an audit and review

the audit to provide assurance and audit-related services." Goal - the

establishment of policies and procedures with respect to those companies in the

organization of the system of quality control. The content presents the main

comments on the development of policies and procedures established for the

quality control tools. The purpose of the third standard - International

Standard on Auditing 220R « Quality Control audit and reporting financial

information " is to establish requirements and issuing professional advice

on the implementation of quality control procedures for audit. The content of

this standard refers to the implementation of the principles of quality control

for each audit assignment and on the requirements of the clients of the audit firm.

The listed document contains mandatory section, which reflects the key terms

used in the framework of a standard or regulation. Russian developed approaches

to performance assessment requirements of auditing standards the

self-regulating organizations of auditors are the basis of these documents as

well as the formation of new parameters estimates and methodology. Relying on

international methods for quality control of audit services, the Russian

auditing standards allow to achieve objectivity in terms of the audit opinion

on the reliability of the accounting (financial) statements.

Bibliography

1.

Internet resource resource. Russian

Collegium of Auditors , the access mode - http://www.rkanp.ru

2.

Internet resource . Institute of

Professional Accountants of Russia , the access mode - http://www.ipbr.org/

3.

Internet resource resource.

International Standards on Auditing , the access mode -http :/ / www.nnre.ru

4.

Erokhina E.I. thesis "

Development of approaches performance assessment requirements of auditing

standards SROA members ", Moscow, 2013.